Market Recap – Week Ending August 12

Market Recap – Week ending Aug. 12

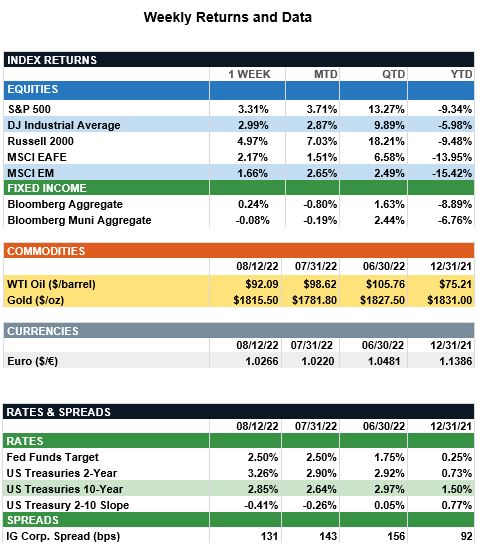

Overview: Stocks rallied last week after data showed signs that inflation, while still elevated, has started to slow. In the U.S., the S&P 500 index finished the week 3.3% higher, while international stocks (MSCI EAFE) rallied about 2.2%. After suffering steep losses earlier this year, small cap stocks outperformed last week with the Russell 2000 index adding nearly 5% in total return. Bond yields were mostly unchanged for the week, as Federal Reserve officials reiterated they still had work to do with regard to taming inflation. According to Fed Watch data, futures markets now are pricing in about a 60% probability of a 0.50% (50 basis point) rate hike at the Fed meeting next month – a drastic shift from the expected 0.75% (75 basis point) rate just a week earlier. In economic data, retail sales are due out Wednesday. Analysts expect core retail sales to have increased by 0.6% in July following a 0.8% gain in June. In addition, investors will keep a close watch on initial jobless claims on Thursday for potential signs of weakness in the robust U.S. labor market.

Latest Update on Inflation (from JP Morgan): Following a relentless rise in inflation this year, markets finally have been able to breathe a sigh of relief as the July inflation figures were softer than expected. Headline CPI was unchanged month-over-month, whereas the year-over-year figure cooled to 8.5% from 9.1% in June. However, core CPI, which excludes food and energy, rose by 0.3% m/m and was unchanged on a year-over-year basis at 5.9%. Turning to the details, the decline in energy prices was a key driver of this downward surprise, falling by 4.6% from a month prior. “Re-opening” demand seems to be cooling off, too, with airfares and hotel prices easing by 7.8% and 3.2%, respectively, and used car prices also falling by 0.4%. On the other hand, food and shelter inflation remain persistent. Food prices increased by 1.1% m/m and owner’s equivalent rent increased by 0.6% m/m. These numbers will be important to watch going forward, as food and shelter account for nearly 45% of the consumer price index and have a significant impact on inflation expectations. The Federal Reserve will take note of this decline, but at best it offsets the very hot July jobs report. Furthermore, while inflation is expected to trend lower, it is unlikely to return to the Fed’s target anytime soon. As such, a data-dependent Fed likely will continue to tighten policy into the end of 2022, and the market’s expectation for rate cuts next year seems a bit misplaced.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.