Market Recap – Week Ending August 19

Market Recap - Week Ending Aug. 19

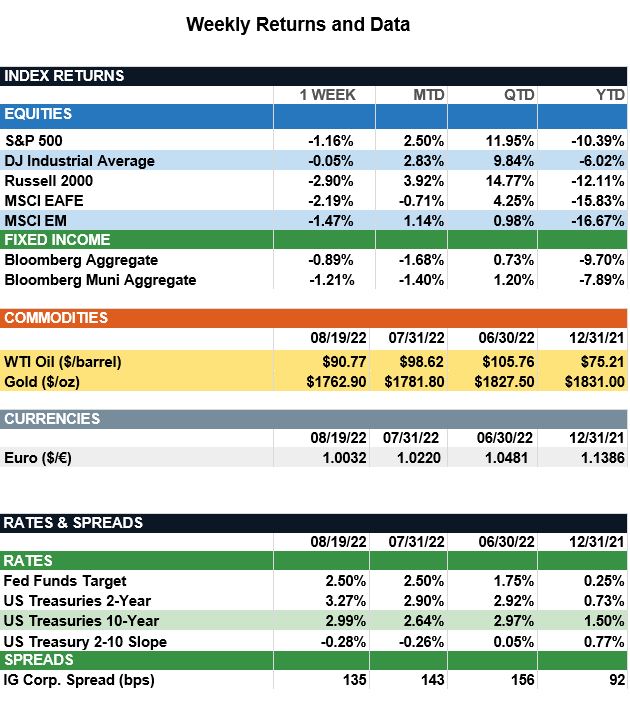

Overview: Stocks traded lower last week, as minutes from the July Federal Open Market Committee (FOMC) noted weaker economic growth amid tighter financial conditions. Despite positive consumer data that showed core consumer spending rising in July, the S&P 500 index finished 1.2% lower for the week. International stocks were lower as well, with international developed (MSCI EAFE) and emerging markets (MSCI EM) down 2.2% and 1.5%, respectively. In bonds, the 2-year Treasury held steady to finish the week at a yield of 3.27%, while the 10-year rose 0.14% (14 basis points) to 2.99%. As markets continue to focus on inflation, key events this week will be a speech from Federal Reserve Chair Jerome Powell on Friday at the Jackson Hole Economic Symposium, as investors look for clues on further interest-rate hikes and guidance for the remainder of the year. On the data front, personal income and outlays are reported on Friday. This report includes the PCE Price Index for July, which is the preferred measure of inflation used by the Fed. Expectations are for the headline PCE price index to fall from 6.8% in June to 6.3% for July, with the Core PCE Price Index expected to fall from 4.8% to 4.7%.

Update on Housing (from JP Morgan): It will be key to see when this weakness in housing begins to translate to decelerating shelter inflation, which would allow core inflation to decrease more sharply. Nowhere in the economy has the surge in interest rates been more important than in the housing market, where the average 30-year fixed-rate mortgage rate rose from 3.0% this time last year to 5.4% this week. This, along with dramatic home price increases, has boosted the average monthly mortgage payment up $627 y/y. In response, this week’s housing data weakened and revealed a further slowdown. July housing starts fell more than expected, contracting 9.6% to a seasonally adjusted annual rate of 1.446 million, the lowest level since August 2020. Building permits (a leading indicator of housing starts) slightly beat expectations, but also fell 1.3% to 1.674 million, suggesting further weakness ahead. In addition, the NAHB’s Housing Market Index, which is designed to measure the pulse of the single-family housing market, dropped to 49 in August, marking the first dip below 50 since May 2020. Investors have embraced the narrative there is a “dovish Fed pivot” coming in the fall, yet this will be largely dependent on how fast inflation cools from here. While housing is important to economic growth overall, it is also critical for inflation. It will be key to see when this weakness in housing begins to translate to decelerating shelter inflation, which would allow core inflation to decrease more sharply. Shelter, accounting for a third of headline CPI, was one area of substantial inflationary pressure in the July CPI report. Shelter costs were up 0.5% during the month, likely stemming from these higher mortgage costs weighing on landlords. According to research from the Council of Economic Advisors, it has historically taken 16 months for weakness in housing to translate to lower shelter inflation, although the particular supply and demand imbalance this time around may prolong this lag.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.