Market Recap – Week Ending Sept 9

Market Recap – Week Ending Sept. 9

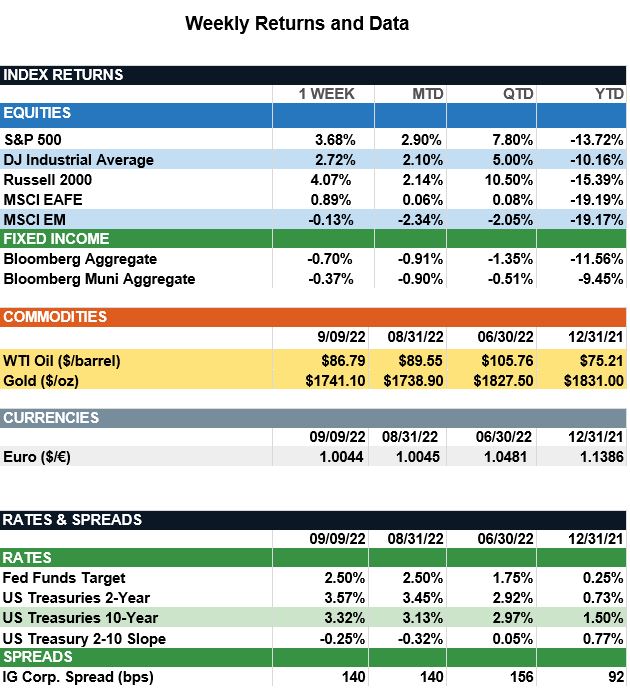

Overview: U.S. stocks rallied last week as Federal Reserve Chair Jerome Powell reaffirmed the Federal Reserve’s focus on bringing down inflation through continued interest rate increases. The S&P 500 index led global stocks, up 3.7% for the week. Futures markets now are pricing in about a 90% probability of a 0.75% rate hike at the Sept. 21 Fed meeting. Yields across the Treasury curve have risen, as market participants price in rate increases expected to take short rates to the 3.75%-4.0% range by year-end. In bonds, the U.S. 2-year and 10-year Treasury yields finished the week at 3.57% and 3.32%, respectively. In Europe, the European Central Bank (ECB) raised their key policy rate by 75 basis points, taking the benchmark deposit rate to 0.75%, the highest level since the year 2011. The ECB indicated it expects to raise interest rates further in an attempt to curb inflation pressures in Europe. In economic data, attention will be focused on the consumer price (CPI) report due out Tuesday, Sept. 13. Headline CPI was 9.1% in June and 8.5% in July, and consensus expectations are for reported inflation to fall to 8.0% for August. This report will be closely watched as the Federal Reserve continues to evaluate data to determine future monetary policy.

Unemployment and Job Openings (from JP Morgan): As economic growth slows this year, a key question for investors is whether job openings can fall from their historical highs without a substantial rise in unemployment. This relationship between job vacancies and unemployment is captured in the Beveridge curve, a downward sloping curve shaped like a skateboard ramp. In expansionary periods, job vacancies tend to be high while unemployment is low, and the labor market moves up the steep part of the curve. During recessionary periods, unemployment is typically high while vacancies are low, and the labor market slides back down to the flat part of the curve. Meanwhile, changes in the efficiency of the job-matching process will shift the entire curve outward or inward, which seems to characterize the post-pandemic recovery. Large shifts in demand patterns, child-care challenges, pandemic aid and job reallocation toward industries that support remote work and away from in-person services all have likely contributed to a decrease in job-matching efficiency. As the Fed seeks to cool an overheating labor market to ease wage pressures, our position on the steep part of the Beveridge curve implies vacancies can fall a good deal without a significant rise in unemployment, increasing the odds of a soft landing. However, the outward shift of the curve also underscores new challenges in job matching in the post-pandemic economy. If this is the case, vacancies may be unlikely to drop much further without a substantial increase in unemployment. In the meantime, tight labor market conditions due to scarce labor in certain industries and regions could keep wage growth elevated and cut into profits in those sectors.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.