Market Recap – Week Ending Sept. 1

Stocks Higher Last Week; Inflation Data Shows Slowing Economy

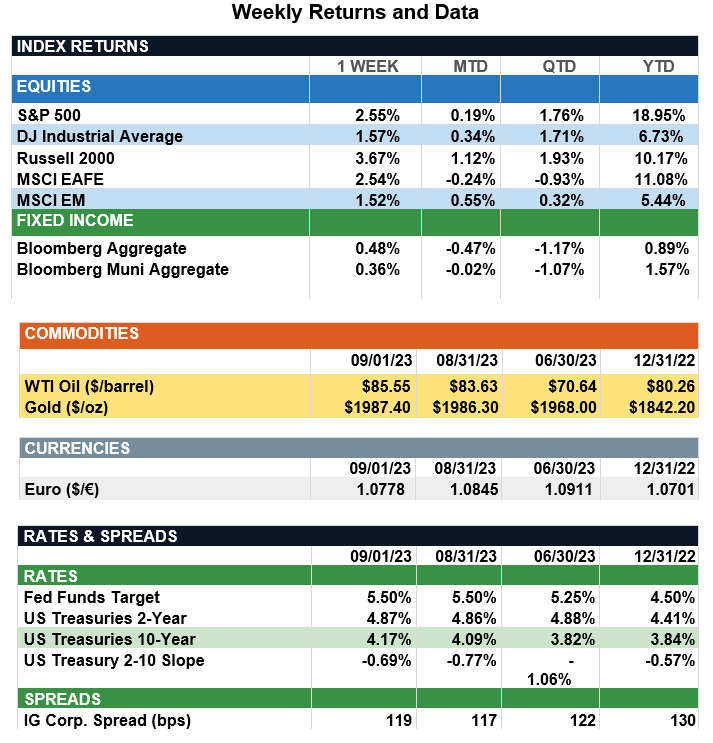

Overview: Stocks finished higher across the globe last week with the S&P 500 index and international developed stocks (MSCI EAFE) both higher by 2.6%. In the U.S., the S&P 500 index recorded its best weekly return since June as inflation data showed the smallest monthly gain in more than two years. In addition, weak job opening data and downward revisions to second-quarter GDP reinforced a slowing economy. This further supports investor expectations the Federal Reserve will hold rates steady at the upcoming Sept. 20 meeting. Fedwatch futures data now is pricing in a 93% chance of the funds rates to remain at the current 5.25%-5.50% range at the meeting. The current market rally in stocks is being driven, at least in part, by the expectation the Fed can continue to bring inflation down while avoiding a recession. Recent economic data has supported this theme, with second-quarter GDP revised downward and inflation continuing on a downward trend. On the jobs front, revisions for payrolls for June and July were revised down by a combined 110,000, and the unemployment rate increased from 3.5% to 3.8%, evidence the labor market is showing signs of slowing.

Update on Trade Relationships (from JP Morgan): Since the onset of the pandemic, “nearshoring” (moving offshore manufacturing closer to the U.S.) and "friendshoring" (moving offshore manufacturing to places that have strong diplomatic relations with the U.S.) have garnered more interest. Russia’s war in Ukraine, tensions between the U.S. and China, new tariffs and changes in relative manufacturing wages also are responsible for building this trend. Evidence of these supply-chain rearrangements is beginning to be reflected in trade-flow data. Remarkably, China no longer is the U.S.’s largest source of goods imports for the first time since 2008, with both Mexican and Canadian imports surpassing those from China in 1H23. Although U.S. companies still are highly dependent on Chinese manufacturing, this shift in the U.S.’s trade relationships is serving to highlight other regions’ advantages. Countries in Latin America and emerging Asia, such as Mexico, India, and Vietnam, are benefiting from their lower costs, integration in global supply chains and friendly relations with the U.S. The excitement around “nearshoring” has boosted Mexican equity markets and peso vs. USD this year, up 25.4% and 14.0%, respectively. Notably, Mexico’s automotive industry received record FDI inflows of US$5.0B in 1H23. In India, the government is making “friendshoring” more attractive by reducing corporate taxes for new manufacturing production to 17% from 25% and making significant investments in infrastructure. Vietnam shares a similar pro-growth attitude and also has very favorable manufacturing wages. While the future of this trend is uncertain, investors can participate by further diversifying emerging market exposure with a focus on the potential beneficiaries.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.