Market Recap – Week Ending Sept. 15

Stocks Mixed; Federal Reserve Meeting This Week

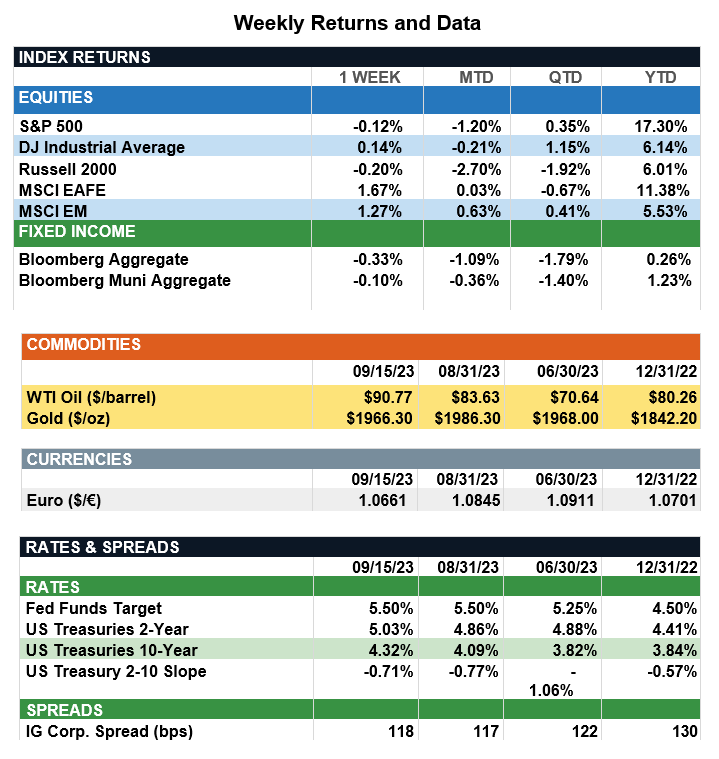

Overview: Stocks were mixed across the globe last week, led on the positive side by international developed stocks (MSCI EAFE) and emerging markets (MSCI EM) which were higher by 1.7% and 1.3%, respectively. In the U.S., the S&P 500 index initially traded higher after strong retail sales data surprised on the upside, then traded lower Friday in response to the auto workers strikes. For the week, the S&P 500 index finished lower by 0.1% as markets now look forward to this week’s Federal Reserve meeting. With the Fed widely expected to leave rates unchanged when the meeting concludes on Wednesday, Sept. 20, the 2-year and 10-year Treasury notes finished the past week at yields of 5.03% and 4.32%, respectively. We believe current interest rates price in expectations the Fed tightening cycle is nearing an end, as markets now anticipate the central bank to begin easing rates sometime around the middle of next year. As the Fed monitors growth and inflation metrics, consumer spending remains robust as retail sales rose 0.6% month-over-month in August, well above the consensus of 0.1%. On the inflation front, headline consumer price (CPI) rose from 3.2% in July to 3.7% in August, with energy prices contributing significantly to the increase (see next paragraph).

Update on Inflation and the Federal Reserve (from JP Morgan): According to Federal Reserve Chairman Jerome Powell, the Fed “is navigating by the stars under cloudy skies.” In the wake of this admission that the outlook is not terribly clear, investors turned their attention to the August CPI report, hoping for a better view of what might lie on the horizon. While the report revealed an acceleration in price growth, it was largely in line with expectations. Headline CPI climbed 0.6% m/m and core CPI rose 0.3% as some prior disinflationary forces reversed course. The key question is how long will these factors provide an inflationary impulse? The details of the report revealed energy prices were a significant contributor to the August acceleration, accounting for more than half of the increase in headline CPI. Specifically, gasoline prices surged by 10.6% m/m, a consequence of production cuts by OPEC+ and increasing refinery margins. However, food prices edged up by a modest 0.2% m/m, and excluding volatile food and energy, the three-month annualized core CPI stands at 2.4% y/y; this reflects the progress made bringing inflation back to its target level. Looking ahead, an ongoing slowdown in Europe and expansion of refining capacity suggest further surges in gasoline prices are unlikely. Additionally, core services, helped by cooling rents and wages, should lead to further moderation. This week, we expect the Fed will leave policy rates unchanged as the futures market are pricing in a less than 5% probability of a hike. Furthermore, the Fed’s commitment to a data-driven approach likely is to be reiterated. However, investors should note central bank policy is becoming increasingly dispersed, and this deviation from the synchronized rate hikes seen in 2022 could lead volatility to rise into the end of the year.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.