Market Recap – Week Ending Sept 16

Stocks Sharply Lower after CPI Report

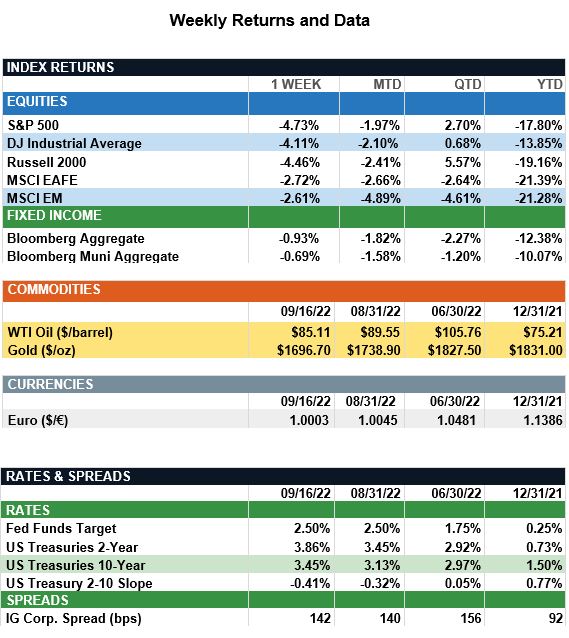

Overview: Global stocks traded lower last week amid ongoing angst that central banks around the world will continue with aggressive monetary policy in raising interest rates to fight inflation. In the U.S., the S&P 500 fell 4.7% following a higher-than-anticipated report on consumer prices (CPI). In the bond markets, yields increased sharply last week on the heels of the inflation report, as market expectations now are for the Federal Reserve to raise rates by at least 0.75% (75 basis points) at their policy meeting this Wednesday (Sept. 21). The U.S. 2-year Treasury yield finished the week at 3.86%, up from 3.45% at the beginning of September, as markets price in expectations of a 4.00% - 4.25% funds rate by year-end 2022. In economic news, the U.S. August consumer price index (CPI) rose 8.3% annualized and 0.1% month-over-month. The increase was larger than consensus expectations, as high food prices and rents continue to pressure inflation. Market focus this week will be on the Federal Reserve meeting concluding on Wednesday, as investors look for guidance on future policy.

Update on Inflation (from JP Morgan): By the end of the summer, investors had adopted a view inflation would decelerate at a healthy pace into the end of the year. While headline CPI did decelerate to 8.3% y/y in August on the back of a 5% decline in energy prices, the report disappointed on a month-over-month basis as inflation rose 0.1% m/m versus expectations for a sequential decline. While some of the disappointment in the headline figure stemmed from food prices rising 0.8% during the month, the core figures were a bit unsettling, rising 0.6% in August and 6.3% y/y. In the details, inflation in core services outpaced inflation in core goods, and shelter costs continued to move higher. Despite this disappointing report, we see reason to expect prices will continue to cool in the coming months. Food, energy and other commodities prices had been growing faster than the headline number itself but are finally starting to come down. This is key, as together these items account for 40% of the CPI basket. Looking ahead, we expect commodity disinflation to spill over to other categories. This notion was reinforced by the 0.1% m/m decline in producer prices, which should eventually feed into lower CPI. Futures markets responded to the inflation release by fully pricing in a 75bp rate hike at the Fed’s meeting this week, with some financial participants even positioning for a full 1% rate hike. We expect the Fed will deliver 75bp of tightening this month and continue hiking into the end of 2022. Fundamentally, this inflation report creates more uncertainty around the trajectory of rates, and that wider distribution of outcomes will continue as a source of indigestion for risk assets until there is more clarity on the broader direction of inflation.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.