Market Recap – Week Ending Sept 2

Market Recap – Week Ending Sept. 2

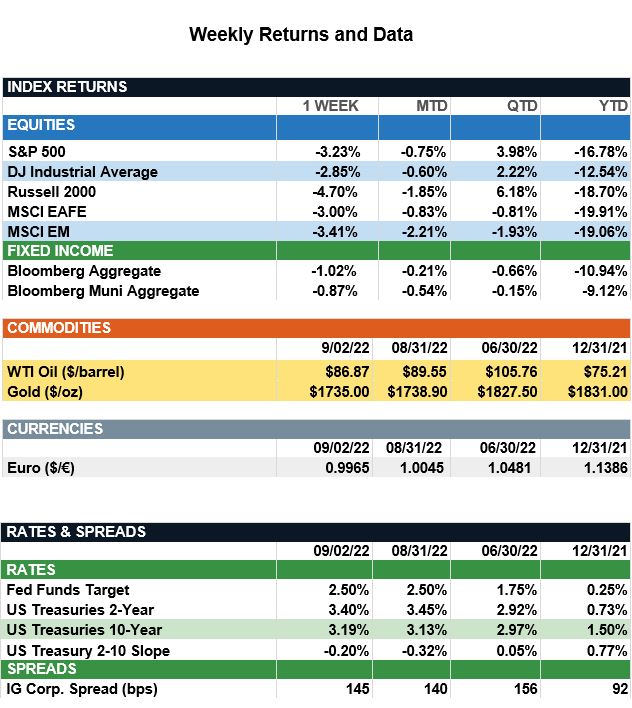

Overview: Global stocks were lower last week on the heels of strong U.S. employment and manufacturing data, as investor concerns continue over inflation and aggressive rate hikes by the Federal Reserve. In the U.S., the S&P 500 index finished the week 3.2% lower, with international developed stocks (MSCI EAFE) and emerging markets (MSCI EM) down 3.0% and 3.4%, respectively. In bonds, the 2-year US Treasury rose to a 14-year high mid-week on concerns of further rate hikes by the Fed before finishing the week at a yield of 3.4%. The 10-year Treasury yield rose to 3.19%, leading to a negative weekly return of 1.0% for the aggregate benchmark of taxable bonds. In economic data, the monthly employment report showed resilient job markets with nonfarm payrolls increasing 315,000 in August, above the consensus of 293,000. Meanwhile, the unemployment rate increased from 3.5% to 3.7%. As we enter the final stretch of the year, attention now turns to the consumer price (CPI) report due out Sept. 13. Headline CPI was 9.1% in June and 8.5% in July, and markets will look for continued improvement in reported inflation as the Federal Reserve continues to evaluate data to determine future monetary policy.

Update on Markets (from JP Morgan): From bonds (U.S. Fixed Income -2.8%, Global High Yield -1.5%) to equities (U.S. Large Cap -4.1%, U.S. Small Cap -2.0%) to commodities (Bloomberg Commodity Index +0.1%), major asset classes disappointed across the board in August. Nearly every market is being driven by the path of central bank policy and its impact on the economy. While investors were hopeful for dovish signals at the Fed meeting in Jackson Hole, Wyoming, they were forced to readjust their summer expectations from a dovish pivot to a Fed strategy of “hike and hold” next year. Accordingly, markets now are pricing in a 70% likelihood of a 75-bps hike in September, followed by a 50-bps hike in November and a 25-bps hike in December, bringing the year-end federal funds rate range to 3.75-4.00%. Expectations for rate cuts in 2023 were pushed back, as markets brace for higher rates for a longer environment. Treasury yields also have factored in this continued hawkishness with the 2Y hitting 3.5% last week, its highest level since 2007. Summer may be drifting away, but volatility is here to stay this fall. From European energy woes to China COVID-19 zero policy to the Russia/Ukraine war to recession speak, investors have a lot to grapple with. The only real certainty is global central banks remain laser focused on taming inflation and are willing to sacrifice some softness in the economy and labor market to do so. Against this backdrop, investors should be prepared for near-term volatility by focusing on defensive positioning and valuations that could favor long-duration bonds, value stocks and income-generating alternatives over more aggressive investments.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.