Market Recap – Week Ending Sept 23

Higher Interest Rates Fuel Concern Over Economic Slowdown

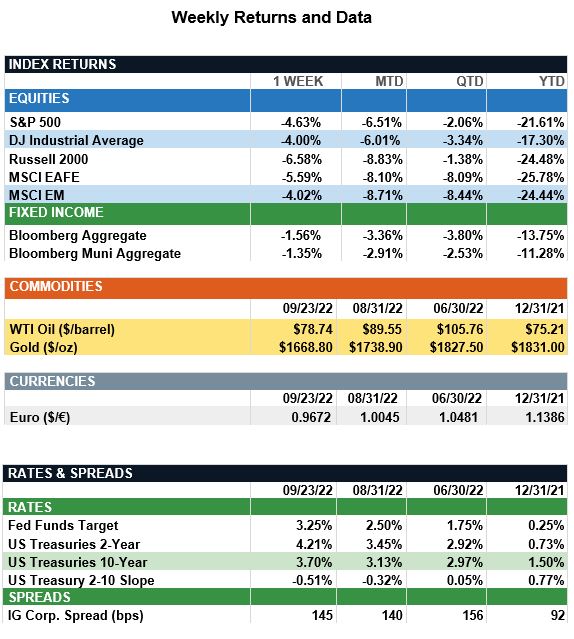

Overview: Global stocks fell sharply last week as higher interest rates fueled concerns over a global economic slowdown. In the US, the S&P 500 fell -4.63% on the heels of the Fed’s 0.75% (75 basis points) rate hike and expectations of aggressive policy for the remainder of the year. International stocks underperformed as well, with the MSCI EAFE falling -5.59% amid an escalation in rhetoric in eastern Europe. Bond yields rose last week as central banks around the globe continued tightening monetary policy. In the US, the 2-year and 10-year Treasury notes both notched 11-year highs, finishing the week at 4.21% and 3.70% respectively. Meanwhile, the U.S. dollar index hit a fresh 20-year high against a basket of global currencies, rising 2.76% on the week. On the data front, investors will be looking forward to housing data, which includes new home sales on Tuesday followed by existing home sales on Wednesday. In addition, the PCE Price Index (Fed’s preferred measure of inflation) is due out on Friday, where core prices are expected to have risen by 4.7% year-over-year in August.

Corporate Earnings Outlook: (from JP Morgan) As of Friday’s close, large-cap equities are down 21.6% YTD. This is more than explained by declining P/E multiples, as earnings expectations themselves have proven relatively robust, despite increasing recession concerns. While wage and input costs have increased rapidly in 2022, analysts’ earnings expectations for 2022 and 2023 have only seen marginal declines since the beginning of the year. This relatively mild reaction to recession fears highlights the perceived ability of companies to pass on higher costs to consumers.

Looking ahead, concerns regarding a slowing economy and rising costs have increased; however, 2023 earnings expectations have remained robust, still pointing to 8% year-over-year growth next year. With this in mind, many investors have quite reasonably been concerned that these expectations are still too high, given the rocky macro outlook. As supply and demand normalize, energy prices are expected to fall somewhat from elevated levels, leading to lower profits in the energy sector in 2023. Additionally, declining job growth and fiscal drag could further crimp consumer spending. Rising interest rates will also be a headwind for corporate profits, both by directly increasing the interest expense faced by companies and indirectly by elevating the dollar. These effects would be further amplified of course, if tight monetary policy were to tip the U.S. economy into recession. A more realistic view of the macro outlook suggests that analysts will probably cut their expectations of future earnings some more, partially validating some of the weakness we’ve seen in equity markets so far this year. However, stocks are a long-term investment; and while earnings may face challenges, earnings should recover in 2024 and beyond, supporting a rebound in U.S. equities from today’s depressed levels.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.