Market Recap - Week Ended Sept. 29

Congress Passes Short-Term Funding Bill; Rising Interest Rates Drive Bond Prices Lower

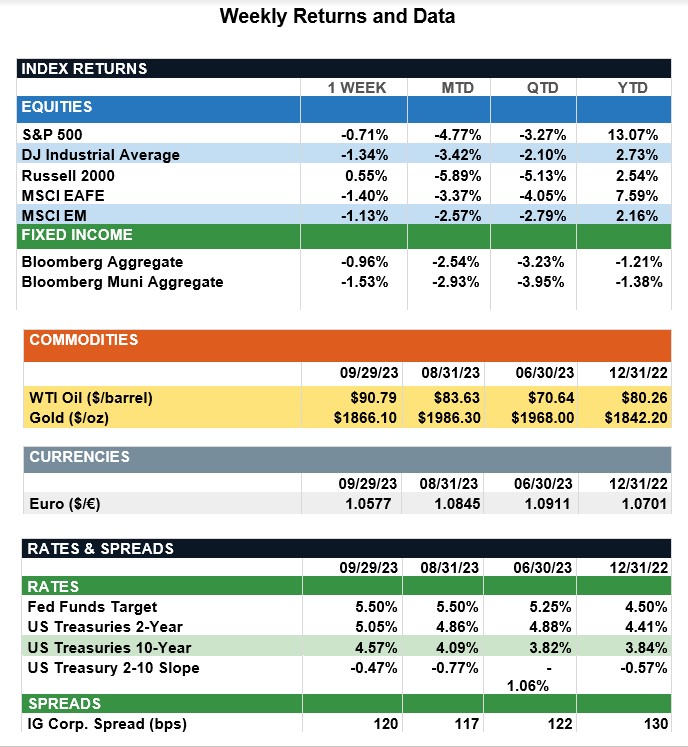

Overview: U.S. equities fell last week on concerns that interest rates will remain elevated for longer, along with fears of a government shutdown. In the final hours of September, Congress passed a short-term funding bill and avoided a shutdown, with funding lasting until November 17th. The S&P 500 index was down 0.7% for the week, finishing its worst month of the year, down about 4.8% in September. In the bond markets, returns for both the Bloomberg Aggregate taxable and municipal bond indices turned negative for the year, as rising interest rates have driven bond prices lower. The 10-year Treasury note finished the week at a yield of 4.57% on the week, higher in yield by about 0.5% (50 basis points) for September alone. On the inflation front, the Federal Reserve’s preferred measure of inflation, the core PCE Price Index, declined from 4.3% to 3.9% year-over-year for August, reflecting a slowing improvement of inflation. Meanwhile, GDP growth for the second quarter was unchanged at 2.1%, and the latest estimate for third-quarter GDP from the GDP Now metric (Atlanta Fed) is 4.9%. The Fed will continue to monitor growth, labor market strength and inflation metrics as it considers any further interest rate increases. Futures markets, according to FedWatch data, now are pricing in about a 50/50 chance of one additional 25-basis-point rate hike by the end of the year.

Update on Market Returns (from JP Morgan): Resilient economic activity during the third quarter helped spur excitement for a “soft-landing” of the U.S. economy. However, the quarter was less exciting for financial markets, which struggled as investors re-positioned for higher rates for longer. In fact, of the nine major asset classes, only two saw positive gains. Commodities had a strong quarter, finishing up 4.7%. This gain can be attributed to higher energy prices, which jumped as supply cuts from Russia and Saudi Arabia raised concerns of an imbalance in the oil market. The U.S. fixed income market struggled as yields climbed (10-yr yields +73bps QTD) to their highest levels since 2007 due to continued hawkishness from the Fed on the back of strong economic data and hefty supply coming to market. However, resilient earnings and a slight moderation in default rates helped spare global high yield from the broader market sell-off. Within the U.S. equity market, large and small caps were down, as the AI driven rally earlier in the quarter left valuations stretched and proved to be unsustainable. Additionally, while earnings came in stronger than expected, corporate guidance was pessimistic. In international markets, a stronger U.S. dollar and weakening growth in Europe and China weighed on returns, with DM and EM equities down by 4.0% and 2.8%, respectively. However, India and Japan were bright spots, with both countries outperforming their respective indices. Moving forward, as economic tailwinds fade and headwinds build along with tighter monetary policy, investors should continue to diversify. Moreover, some asset classes still look expensive despite this quarter’s sell-off, and investors should use active management to lean into underappreciated asset markets.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.