Market Recap – Week Ending Sept 30

Markets Remain Focused on Inflation and Interest Rates

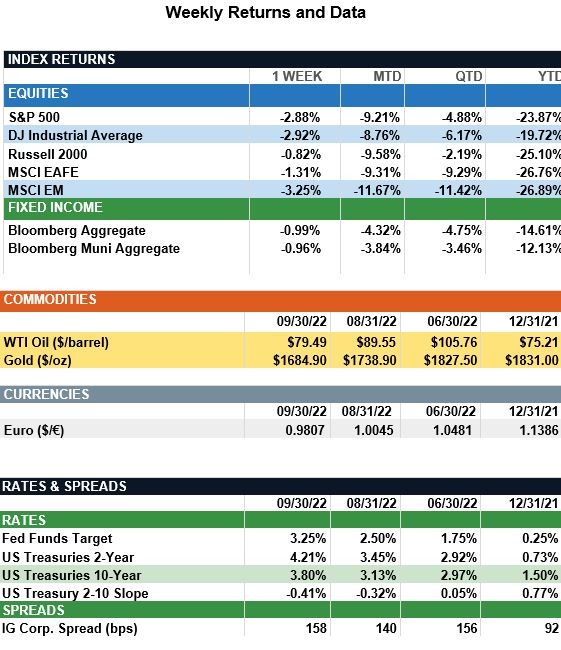

Overview: Global stocks are coming off another tough month with the Dow Jones and S&P 500 both notching their biggest monthly losses since March of 2020. The Dow shed 8.8% in September while the S&P 500 fell 9.3% for the month. Despite better-than-expected jobless claims last week and improving consumer sentiment, markets remain focused on the outlook for interest rates and inflation. In the U.S., Core PCE came in above consensus at 4.9% for August, driven primarily by consumer spending. In the Euro Area, CPI inflation data last week showed prices rose by 10% year over year, well above forecasts. On the housing front, sales of new single-family homes increased by 28% in August even as mortgage rates hit new highs for the year. On the other hand, the housing market is showing signs of normalization as July home prices fell for the first time since 2012. Going forward, markets are pricing in approximately 1.25% of rate hikes for the remainder of the year, which would lead to a fed funds rate around 4.5% by year-end.

Fourth-Quarter Outlook (from JP Morgan): The third quarter of 2022 saw financial assets continue their year-to-date decline, as positive stock-bond correlations and a pullback in commodity prices delivered negative returns across all asset classes except cash. A third consecutive rate hike of 75bps from the Fed piled further pressure on bonds, with U.S. fixed income markets down 4.8% in 3Q22. Additionally, the combination of rising rates and growing concerns around a policy error leading to recession led global high yield to decline 2.7% in the third quarter. Although credit quality has remained relatively stable this year, slower growth, persistent inflation, and higher rates could increase credit risk over the next few months. Turning to equities, U.S. large cap and small cap equities found little relief in 3Q22, as a further deterioration in multiples and declining earnings expectations led to negative returns. In international markets, developed market equities fell 9.3% as European markets continue to be challenged by higher energy costs and a negative reaction to the U.K.’s recent fiscal and monetary policy. In emerging markets, equities were down 11.4% as rising inflation across geographies and questions about China weighed on returns.

Although 4Q22 looks set to be another tough quarter for public markets, investors should not be overly pessimistic. S&P 500 forward multiples are currently ~9% below their long-term average, while high-quality fixed income valuations are currently sitting at 10-year lows. These attractive valuations, coupled with elevated interest rate and equity volatility, should be welcomed by investors, as a combination of the two has historically led to significant long-term investment opportunities.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.