Market Recap – Week Ending Oct. 13

Stocks Higher; Full Slate of Earnings Reports This Week

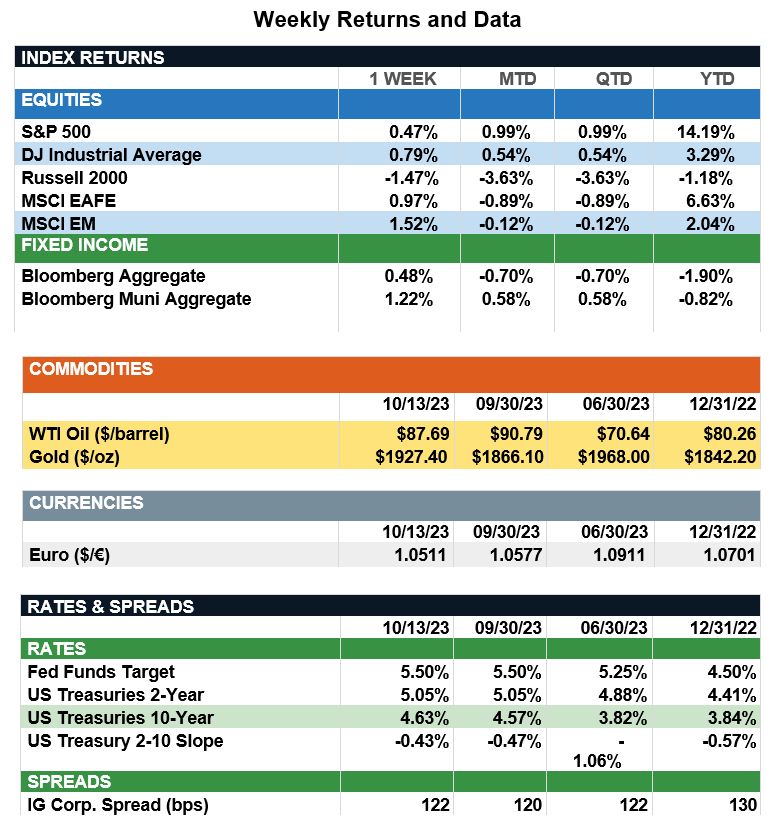

Overview: U.S. stocks finished higher for the second consecutive week with the S&P 500 index up by 0.47% on the week. International stocks followed suit with the MSCI EAFE finishing the week higher by about 1%. Lower bond yields in the first part of the week sent markets higher, while a sticky inflation print on Thursday caused markets to pare some of those gains. Specifically, U.S. headline CPI registered at 3.7% year-over-year for September, above expectations for a more modest 3.6% print. Excluding food and energy, Core CPI showed another move in the right direction, down from 4.3% in August to 4.1% in September. Interest rates remained volatile, particularly on the long end of the curve as investors continue to adjust to the higher-for-longer narrative that recently has taken hold. All told, yield on the 10-year Treasury note finished the week lower by about 15 basis points, trading at a yield of 4.63%. Looking ahead, a full slate of earnings reports this week will give investors a good look at the health of the big banks, airlines, and media companies, among others. According to FactSet, analysts expect earnings for the S&P 500 bottomed out in the second quarter of this year and anticipate third-quarter earnings to show year-over-year growth of around 1.3%. In addition, we expect earnings guidance will be a primary focus for investors, as earnings expectations for the fourth quarter of this year are expected to post double-digit growth of around 11%.

Update on Inflation (from JP Morgan): Headline inflation rose 0.4% m/m and 3.7% y/y in September, partly due to higher energy prices with the gasoline CPI component rising 2.1% m/m and 3.0% y/y. However, there could be better news coming on this front. Last month, the price of crude oil rose to its highest level YTD; however, refining margins actually trended downward, softening the impact of higher crude prices at the gas pump. This reduction reflects a recovery in U.S. and global refinery activity and relatively soft U.S. gasoline demand in September. Moreover, even with the current Middle East turmoil, oil prices now have fallen from their September peaks, suggesting the downward trend in gasoline prices may continue through October and into November. This should help reduce CPI inflation over the next two months, potentially discouraging the Federal Reserve from imposing any further rate hikes and setting the stage for modest reductions in both inflation and interest rates in 2024.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.