Market Recap – Week Ending Oct 14

Volatile Trading Week, Inflation Climbed

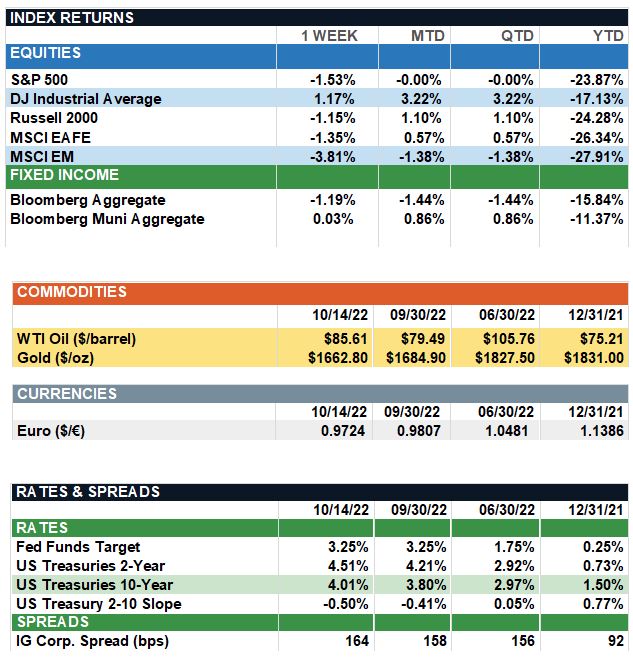

Overview: Stocks experienced another volatile week of trading. At one point, the S&P 500 reached its lowest trading level since November of 2020 before closing the week lower by about 1.5%. Last week, the September Consumer Price Index (CPI) report showed headline inflation climbed 0.4% month over month, missing estimates for a more modest increase. Another large spike in food prices boosted the headline number, which rose 8.2% year over year. In addition, core CPI (which excludes the highly volatile food and energy components) climbed by 6.6% on an annual basis, with the closely watched shelter costs component rising 0.7% for the month. On Friday, retail sales were little changed in September after posting an impressive gain of 0.4% in August. The report cited high inflation and interest rates as the drivers behind the stagnant number. Investors are looking forward to earnings season as well as the Federal Reserve’s meeting on Nov. 2. On the earnings front, investors will look to corporate America for any significant downward revisions to their outlooks in the face of inflation and slowing economic growth. Notable earnings this week include Netflix, Tesla, IBM, and Johnson & Johnson as each will report third-quarter results. In central bank news, the Federal Reserve is largely expected to hike interest rates by another 0.75% (75 basis points) in November. The release of the September FOMC minutes revealed continued policy tightening in the near-term, but an intention to pause rate hikes once interest rates reach a point high enough to reduce overall inflation.

Update on Inflation (from JP Morgan): Following a string of upside surprises, the September CPI report dashed hopes for a deceleration in inflation. Strong services inflation offset declines in core goods and energy prices with Core CPI inflation jumping 0.6% m/m and 6.6% y/y. Wage inflation and resilient demand have contributed to strong services inflation, while the lagged effect of rising rents continues to propel owners' equivalent rent higher. However, the report was not all bad news for investors as disinflationary forces still are contributing to a slowdown in core goods inflation. Softer commodity prices, lower shipping costs and improved supply chains should continue to reduce inflation pressure across a range of goods over the coming months. Importantly, the inventory crunch experienced last year also has reversed. Strong stockpiling in the first half of the year has allowed retail inventories to recover beyond pre-pandemic levels, while retail sales have flat-lined. While this may spell trouble for GDP growth as consumer spending and inventory spending likely are to be very modest going forward, it is good news for inflation as it relieves some of the upward pressure on goods’ prices. For the Fed, the September CPI report, combined with hotter-than-expected wholesale price inflation (PPI) and a strong September Jobs report, gives them little reason to deviate from their recent hawkish forward guidance on rate hikes. We continue to expect the Fed to raise interest rates by 0.75% next month, followed by another 0.50% increase in December. Thereafter, while we may not hear the Fed talk about policy easing for some time, a shift to smaller hikes and then a pause may not be too far off if disinflationary forces continue to weigh more heavily on the data.

Weekly Returns and Data

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.