Market Recap – Week Ending Oct 21

Market Rebounds; PCE Price Index Coming Friday

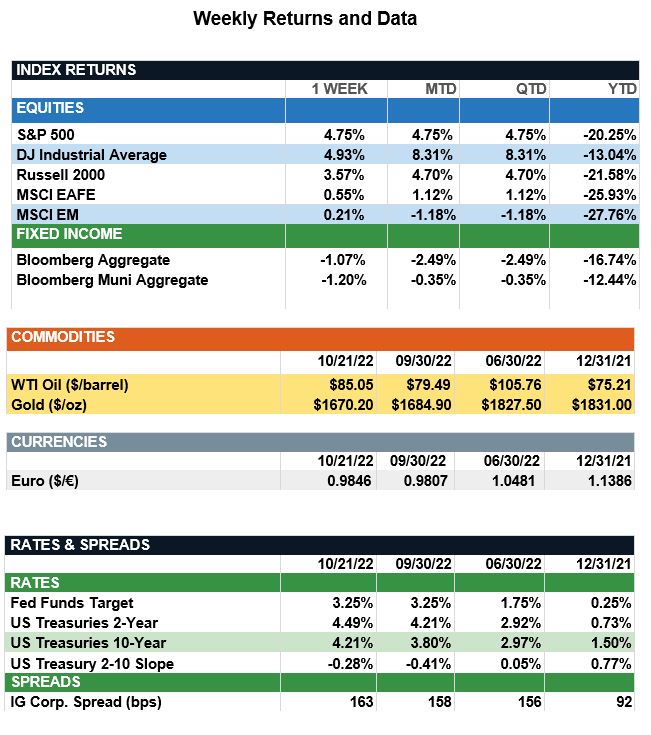

Overview: Stocks across the globe finished higher last week, led in the U.S. by the S&P 500 index, which rose 4.8% on a solid start to the third-quarter earnings season. In the bond markets, market pricing of Federal Reserve policy expectations has continued to put pressure on interest rates as investors react to the Fed’s commitment to aggressive monetary policy to fight inflation. The 10-year Treasury note traded at 15-year highs during the week, finishing at a yield of 4.21% as market expectations now are for an almost certain 0.75% (75 basis point) hike in rates at next week’s Fed meeting, and with expectations of a further hike in rates to around 4.5% by year end. Looking ahead, key data this week will be released on Thursday with the first look at third-quarter Gross Domestic Product (GDP), with consensus expectations for a 2.3% increase for the quarter, vs. -0.6% for the previous quarter. Friday (Oct. 28) we will get data on personal consumption and the PCE Price Index, which is the Federal Reserve’s preferred measure of inflation. Headline PCE is expected to rise from 6.2% to 6.3% on an annual basis, with the core PCE expected to increase from 4.9% to 5.2%. These key growth and inflation metrics will be closely watched by investors and any deviations likely will influence markets direction.

Update on Housing (from JP Morgan): A slowdown in the housing market will drag on economic growth, and with other parts of the economy beginning to slow as well, the risk of a policy error by the Federal Reserve continues to rise. As the U.S. Federal Reserve continues to aggressively tighten monetary policy, the average 30-year mortgage rate has skyrocketed to a two-decade high of 6.94%. These higher borrowing costs, coupled with elevated home prices, have pushed housing affordability down to multi-decade lows and weighed on housing market activity overall. Underscoring this slowdown has been existing home sales, which have contracted every month since the start of the year and fell 1.5% m/m and 23.8% y/y to a seasonally adjusted annual rate of 4.71 million in September. The NAHB Housing Market Index, which measures homebuilder confidence, dropped for the 10th consecutive month to levels last seen during the pandemic. Finally, this weakness also has reflected in housing starts, which fell 8.1% m/m to an annual rate of 1.439 million last month. While U.S. home prices have started to moderate, we do not expect a collapse in the housing market. For one, the inventory of new and existing single-family homes is 1.536 million, well below the long-term average of 2.399 million. Further, leverage in the housing market, as measured by mortgage debt service payments as a percent of disposable income, sits at 3.9%, just more than half of the 7.2% peak seen in 2007. That said, a slowdown in the housing market will drag on economic growth, and with other parts of the economy beginning to slow as well, the risk of a policy error by the Federal Reserve continues to rise.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.