Market Recap – Week Ending Nov. 3

Markets Rebound as Major Stock Indices Have Best Week of 2023

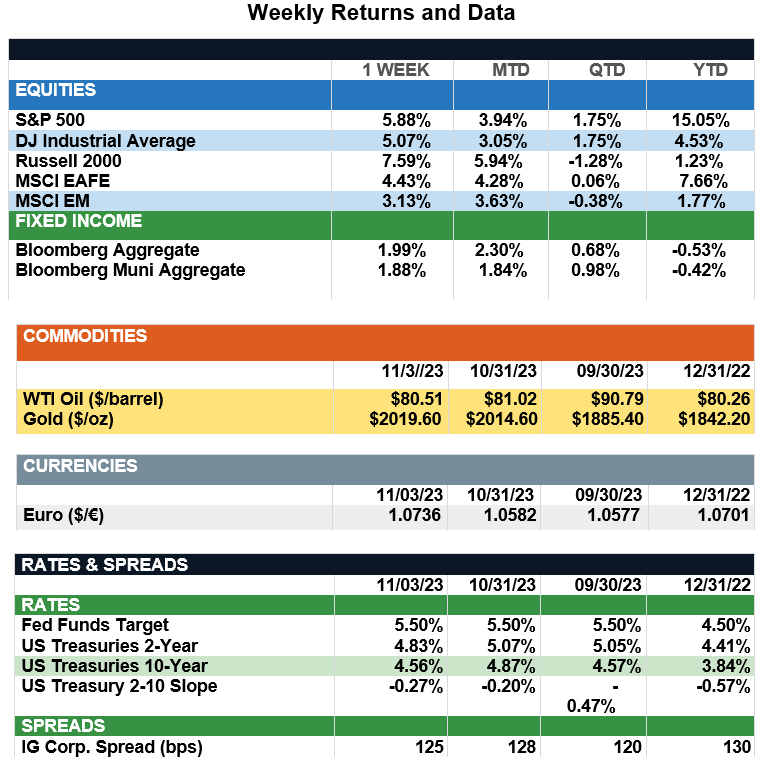

Overview: Stocks and bonds across the globe rebounded last week as the Federal Reserve concluded their November meeting by leaving the target range for the federal funds rate unchanged at 5.25%-5.50%. Investors welcomed a jobs report that showed nonfarm payrolls increased by 150,000 in October, less than expected. Markets are hopeful a cooling labor market is healthy and will continue to support disinflation. Major stock indices in the U.S. responded with their best week of the year 2023 so far, with the S&P 500 index higher by 5.9%, and the Nasdaq Composite up 6.6%, the best week since November 2022 for both indices. International stocks followed suit with developed stocks (MSCI EAFE) and emerging markets (MSCI EM) higher by 4.4% and 3.1%, respectively, on the week. In the bond markets, sharply falling yields led to strong returns for both taxable and municipal bond indices, which were both higher by about 2% on the week. Bond yields fell on optimism the Fed has reached its terminal rate, along with news the U.S. Treasury would slow the pace of issuance of 10- and 30-Year Treasuries relative to shorter-maturity notes. The 2-Year and 10-Year US Treasury yields finished the week at yields of 4.83% and 4.56%, respectively, with the 10-year note falling a full 30 basis points (0.30%) on the week. Looking ahead, highlights for markets will be earnings updates from the likes of Occidental, Walt Disney, Wynn, and MGM, as the third-quarter earnings season winds down. Investors also will continue to look for clues to future Fed policy, as Federal Reserve Chair Jerome Powell is scheduled to speak twice in the coming days.

Update on Labor and Inflation (from JP Morgan): In last Wednesday’s FOMC new conference, Fed Chair Powell acknowledged wage inflation has “come down significantly” but suggested economic and labor market conditions likely need to come further into balance to bring inflation back to target. With this in mind, some may fear continued labor market strength could stall further progress on wage growth and inflation. Importantly, the October Jobs report showed a welcomed decline in average hourly earnings (AHE) to 4.1% y/y, down meaningfully from last year’s peak of 5.9%. That said, while wage growth should normally be above CPI inflation due to productivity gains, 4.1% growth still seems higher than what is consistent with the Fed’s 2% PCE target. However, as pandemic-related distortions continue to recede from the labor market, wage growth could see further moderation even if the labor market remains tight. Prior to the pandemic, shifts in the composition of the labor market, measured by each sector’s share of weekly hours worked, had little impact on wages. However, the labor market shifted rapidly at the onset of the pandemic as lower paying jobs in industries like leisure and hospitality lost share to higher paying sectors, pushing wages ~2% higher than they would have been without this shock. While the impact of this distortion has eased, further normalization could take another ~50 bps out of wage growth if the composition of the labor market returns to its pre-pandemic mix. With wage growth already cooling, additional dampening from a reset in the share of hours worked across sectors will be welcomed by the Fed as a sign that inflationary pressures can moderate despite a tight labor market. This, along with further evidence of a slowing economy, makes it more likely that we have seen the last of Fed rate hikes.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.