Market Recap – Week Ending Nov. 17

S&P 500 Extends Climb; Home Sales, Durable Goods Data This Week

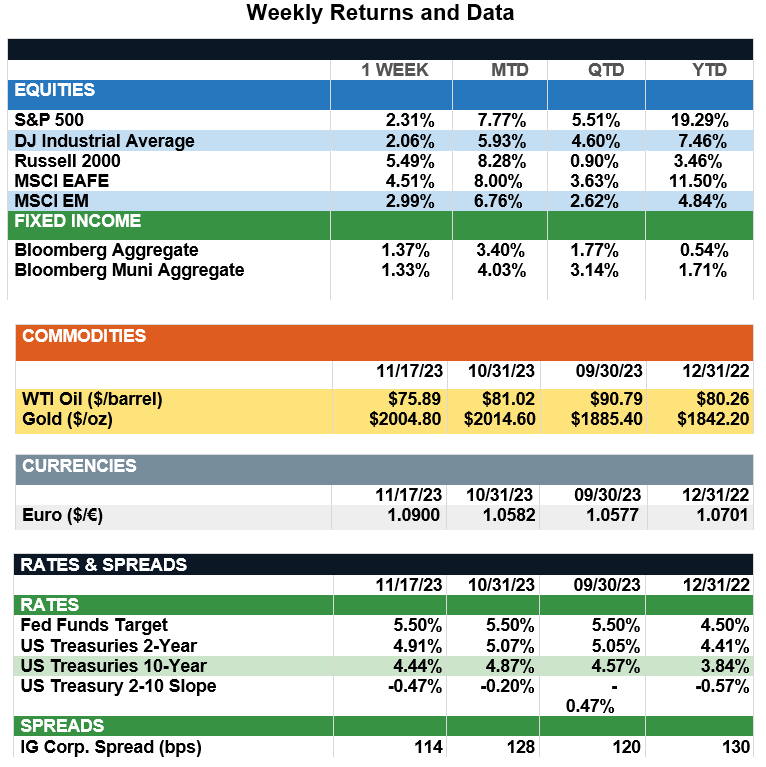

Overview: Stocks were higher across the globe last week, led by international developed (MSCI EAFE) up 4.5%, and emerging markets (MSCI EM) higher by 3.0% for the week. In the U.S., the S&P 500 index ended the week 2.3% higher, notching a third consecutive week of gains. Investors were encouraged by a better-than-expected Consumer Price Index (CPI) report that reinforced hopes the Federal Reserve has concluded its campaign of raising interest rates. Headline CPI decreased from 3.7% in September to 3.2% in October, led by a decrease in energy prices. Meanwhile, core CPI (ex-food and energy) fell to a two-year low from 4.1% in September to 4.0% in October. In the bond markets, yields fell sharply across the Treasury curve as the continuing trend to lower inflation was welcomed by investors. The 2-Year and 10-Year U.S. Treasury yields finished the week at 4.91% and 4.44%, respectively, with the lower rates supporting returns of around 1.3% on the week for both taxable and municipal bond indices. In this holiday-shortened week for the markets, economic data will be light, highlighted by home sales data on Tuesday and durable goods orders due Wednesday. With earning season winding down, an important release will come on Tuesday from Nvidia, the chipmaker that is up over 240% for the year. With markets now expecting no change in rates for both the December and January 2024 Fed meetings, investors will continue to monitor forward guidance from key companies along with economic data for clues to future growth and consumer spending.

Update on Consumer Spending (from JP Morgan): It’s not even Thanksgiving yet, but the holiday spending rush has already begun. The National Retail Federation is forecasting holiday spending growth of 3-4% from 2022, totaling between $957.3-$966.6 billion. This represents a normalization in holiday consumption growth to the pre-pandemic average of 3.6% y/y from 2010-19 after the last three years were impacted by government stimulus. Higher prices and dwindling savings are putting pressure on consumers, but household balance sheets and debt service ratios remain healthy overall. However, holiday spending plans vary significantly between income groups. High-income households still have considerable savings, and those earning +$200K annually are expected to spend 22% more than last year according to Deloitte. Lower-income shoppers may have already depleted their savings but will likely hunt for discounts, use more “buy now, pay later” options and rely on credit to continue spending. Despite expectations for solid holiday spending growth, consumer companies need to be strategic given building headwinds such as increased difficulty in obtaining credit and lower consumer confidence. Those offering discounts and adapting to changes in customer preferences will likely see strong earnings results in 4Q. Looking ahead, consumption is likely to soften further following October’s retail sales decline of 0.1% m/m. More “normal” consumer spending activity in November and December could be favorable for markets and allow the Fed to cut rates earlier in 2024. While investors may want to wait for more data on how the economy is performing, slowly adding exposure to longer duration fixed income and equities is still prudent.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.