Market Recap – Week Ending Nov. 24

Rally Continues; Key Inflation Data Coming Thursday

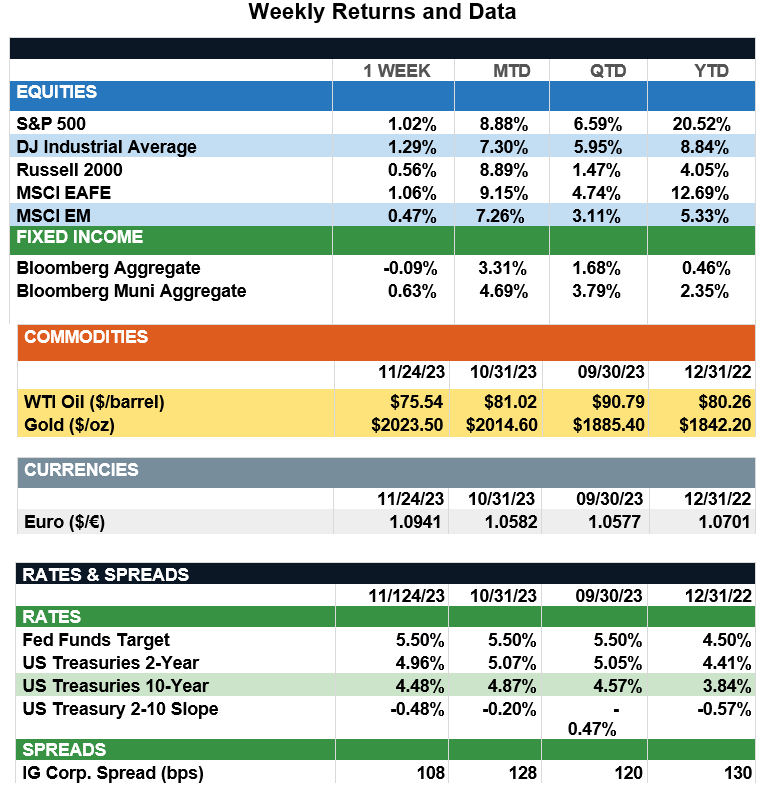

Overview: Stocks around the globe continued their November rally in holiday-shortened trade last week. In the U.S., the S&P 500 index finished up 1.0%, notching gains for the fourth consecutive week. Both international and domestic stocks have recorded strong performance in November with global indices up 7-9% in total return for the month-to-date. Markets have rallied on the back of falling interest rates as the 10-year Treasury yield finished the week at 4.48%, down from the 5% level reached in late October. Investors are hopeful the Federal Reserve is done with its rate-hiking campaign, as futures market data (according to CME FedWatch) is pricing in about an 88% chance rates will remain unchanged, looking forward to the Jan. 31, 2024, meeting. The Federal Open Market Committee (FOMC) minutes from the November meeting showed all participants voted to keep the federal funds rate unchanged, reinforcing the market view that disinflation is continuing toward the 2% target rate of the Fed. Key inflation data this week will be reported on Thursday, when the Fed’s preferred measure of inflation, the Personal Consumption Expenditures (PCE) Index, is reported for October. The headline PCE Price Index is expected to fall from an annualized rate of 3.4% to 3.1%, with the core PCE Price Index projected to decline from 3.7% to 3.5%.

Update on Market Opportunities (from JP Morgan): As Americans gathered around the Thanksgiving table last week and recited what they were thankful for, market performance may have made the list with 60/40 portfolios up 12% this year after a challenging 2022. The path hasn’t been smooth, with a regional banking crisis, war in the Middle East and hawkish Fed policy all challenging markets. However, good news outweighed the bad news, and disinflation, pandemic savings cushions, supported housing prices and new industrial fiscal policies from the Inflation Reduction Act all contributed to economic resilience that surprised many expecting a recession. The biggest surprise though likely was the strength of U.S. large-cap growth against the winds of aggressive monetary tightening. The “Magnificent 7” is up over 70% this year and accounts for 94% of S&P 500 YTD returns. The sudden progression of AI into mainstream culture not only has inspired consumer excitement about the sophistication of AI technologies but also sharpened investment focus, with more than 35% of S&P 500 companies mentioning AI in 3Q23 earnings transcripts and global private investment projected to reach $200bn by next year. Looking ahead, it’s an exciting time to be an investor. AI should remain investable for the long haul, with the rapidly developing AI industry suggesting opportunities will broaden beyond the top seven stocks. For investors wary of overextended markets, there are plenty of stocks that haven’t seen the same run-up in valuations this year, with the remaining S&P 500 only up 3.5% YTD. In short, markets continue to present opportunities for investors either looking to add risk with growth or defensiveness with value, and leaning into active management should allow investors to weather what could be another year of surprises ahead.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.