Market Recap – Week Ending Dec. 1

Stocks Continue Climb; Key Employment Report This Week

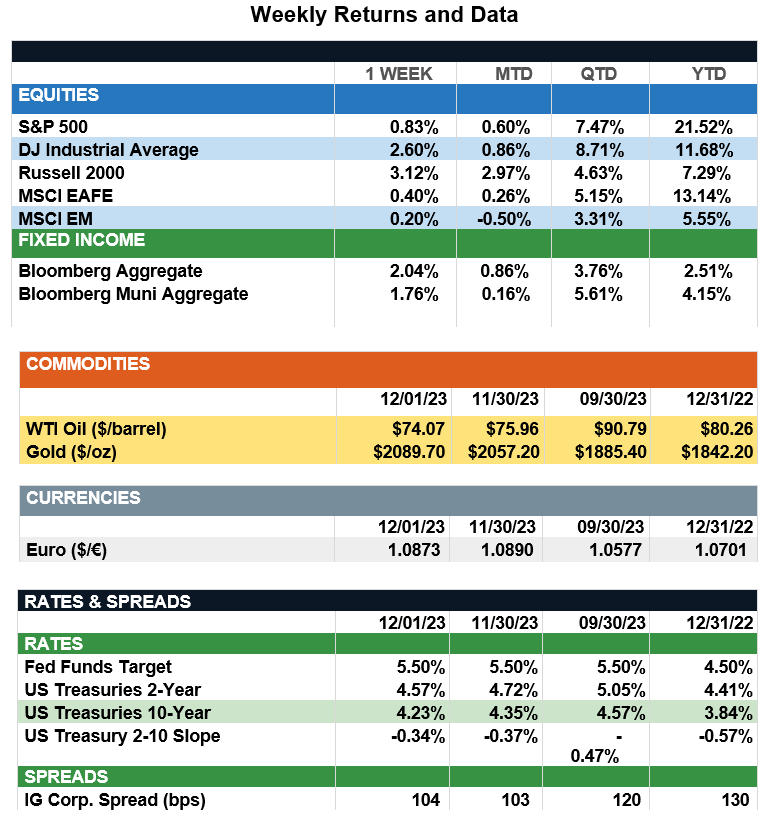

Overview: Stocks traded higher for the fifth consecutive week last week as investors are optimistic the Federal Reserve has finished its rate-hiking campaign. Futures markets, according to FedWatch, are now pricing in more than a 99% probability the funds rate will remain unchanged in the current range of 5.25%-5.50% at the final Fed meeting of the year next week. In the U.S., the S&P 500 Index closed at a new 2023 high on Friday, up 0.8% for the week and up more than 21% year-to-date. Small-cap stocks led the way for the week as the Russell 2000 Index was higher by more than 3%. Stocks have continued to rally, and yields have fallen, though Fed Chair Jerome Powell has repeatedly stated it is “premature” to anticipate any easing in rates. In the bond markets, the 2-Year and 10-Year U.S. Treasury yields fell to their lowest levels in more than two months, ending last week at 4.57% and 4.23%, respectively. The broad-based bond market indices have benefitted from these falling rates, with the taxable and municipal indices higher year-to-date by 2.5% and 4.1%, respectively. In economic news, inflation continues to show a downward trend, as October core personal consumption expenditures (PCE) fell to 3.5%, as progress continues toward the 2% inflation target for the Fed. Key data this week will come on Friday in the form of the monthly employment report where the expectation is for an increase in nonfarm payrolls of 160,000, with the unemployment rate expected to remain steady at 3.9%.

Update on Housing and Consumer Spending (from JP Morgan): Despite a decline over the past few weeks, the 30-year fixed-rate mortgage rate remains at nearly its highest level in 20 years and more than double its level at the start of last year. However, it is important to distinguish between the impact of this rate surge on the housing market and on consumption. There is a large gap between the average rate on new 30-year fixed-rate mortgages and the average mortgage rate for existing mortgage holders. For home buyers, the change in the environment has been dramatic, leading to a very sharp decline in both housing starts and home sales. However, it is important to recognize that fewer than 4% of American households bought a home in the last year. For the vast majority of families who either don’t have a mortgage or have a fixed-rate mortgage, the surge in mortgage rates has had no impact on their financial position. For this reason, while the Federal Reserve has been raising interest rates to slow aggregate demand, real consumer spending has remained strong, with a 2.2% year-over-year increase in October and a strong early start to the holiday retail season. In short, while the Fed’s higher-for-longer interest rate policy continues to undermine the housing market, it is having little impact on consumer spending and today’s housing crunch, unlike the bursting housing bust of the mid-2000s, and does not appear to be of a magnitude that will put the U.S. economy into a recession.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.