Market Recap – Week Ending Dec. 29

Stocks Up to Close 2023; Key Jobs Data on Friday

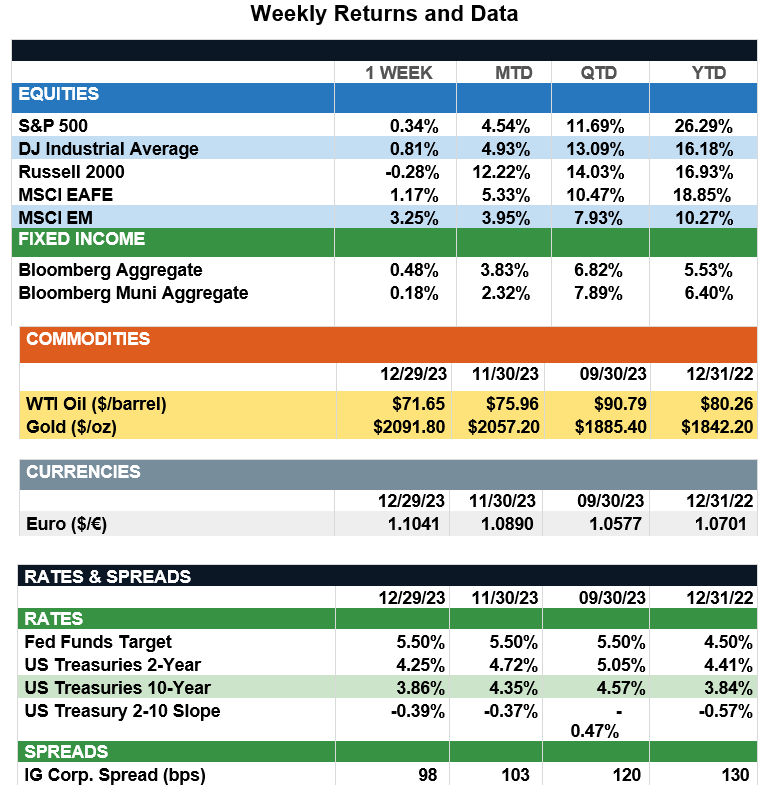

Overview: Stocks closed out 2023 with gains across the globe last week with emerging markets (MSCI EM) up 3.3% to lead the way. In the U.S., the S&P 500 index rose 0.3% to notch its eighth consecutive week of gains. In bonds, Treasury yields fell last week as encouraging inflation data showed continued progress toward the Federal Reserve’s 2% inflation target. The preferred measure of inflation for the Fed, the core personal consumption index (Core PCE) decreased from 3.4% in October to 3.2% in November, beating consensus expectations and bolstering hopes the Fed will ease rates as inflation continues to improve. The 2-Year and 10-Year Treasury yields finished the week at 4.25% and 3.86%, respectively, their lowest close in more than four months. As investors bet the Fed is done with its tightening cycle for rates, lower yields have contributed to a resurgence of total return for both taxable and municipal bonds, with the Bloomberg Aggregate and Municipal bond indexes finishing 2023 up 5.53% and 6.40%, respectively. As investors look forward to the start of 2024, key jobs data will be released on Friday, Jan. 5. Nonfarm payrolls are forecast to rise 158,000 for December, down from 199,000 in the prior month, with the unemployment rate expected to increase from 3.7% to 3.8%.

Update on Market Returns (from JP Morgan): 2023 market returns presented a mirror image to the declines of 2022. Despite recession fears stoked by tight monetary policy, banking sector hiccups and elevated geo-political tensions, all asset classes, save one, experienced positive returns. U.S. Large Cap stocks led the rebound with a 26.3% return as AI enthusiasm propelled mega-cap tech stocks to lofty valuations. Small Cap stocks nearly kept pace, climbing 16.9%, reflecting resilient domestic consumption and beaten-down initial valuations. Turning to international markets, DM equities outperformed their EM counterparts. Corporate governance reforms in Japan, better-than-expected progress on inflation in Europe and resilient earnings boosted DM equities to a 18.9% gain. On the other hand, EM equities ended the year with a 10.3% gain as the downturn in China offset strong gains in Taiwan, India and Korea. Within fixed income, high-yield bonds defied expectations, posting a healthy 14.0% return driven by resilient fundamentals among the underlying securities and an only a moderate increase in default rates. Meanwhile, the broader bond market rallied late in the year with the U.S. Agg. up 5.5% as investors were comforted by the Fed’s dovish shift. Within alternatives, REITs rebounded to a 11.4% gain on the back of strong demand for data centers and hopes for lower long-term rates. Cash, while posting a multi-decade high return of 5.1%, lagged other assets to finish near the bottom of the performance charts. Finally, in a stark reversal from 2022, commodities fell by 7.9%, ending the year as the poorest performer partly due to weaker demand growth from China. For investors, the whipsaw in relative returns from 2022 to 2023 underscores the value of thoughtful active management.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.