Market Recap – Week Ending Dec. 8

Fed Meeting, Key Inflation Data This Week

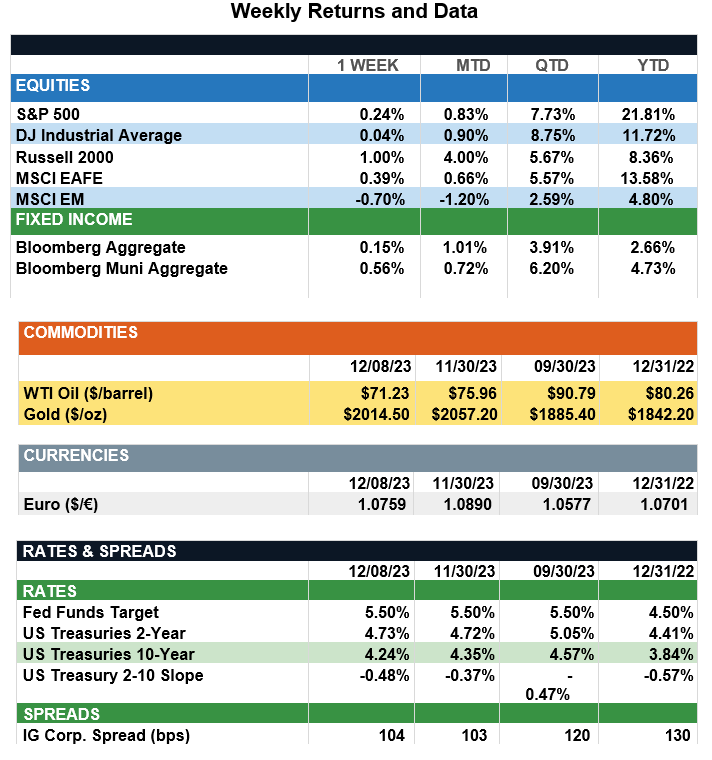

Overview: Stocks across the globe were little changed last week as investors await the results of this week’s final Federal Reserve meeting of 2023. In the U.S., the S&P 500 index was higher by 0.2% on the week. Investors continue to evaluate economic growth and inflation data for any signals for future Fed policy changes. Labor market data was mixed last week, with U.S. job openings falling to a two-and-a-half-year low, signaling declining labor market strength. On the positive side, nonfarm payrolls increased by 199,000 in November, above expectations for a 180,000 increase. The unemployment rate fell from 3.9% in October to 3.7% in November, as the labor market continues to show strength. At the upcoming meeting this week, the Fed is expected to maintain the fed funds rate at the current range of 5.25%-5.5%. Fed Chair Jerome Powell is expected to reaffirm the Fed’s commitment to lowering inflation in his news conference at the conclusion of the meeting. Markets will receive important inflation data this week with consumer prices (CPI) released Tuesday and producer prices (PPI) due out on Wednesday. Headline CPI is projected to fall on an annualized basis from 3.2% in October to 3.1% in November, with core CPI inflation (ex-food and energy) expected to remain steady at 4.0%. In addition, retail sales data will be released on Thursday, representing a checkpoint for consumer spending strength in this holiday season. As investors’ hope for an easing of the funds rate by the Fed, the CME Group’s Fed Watch tool now is indicating about a 40% likelihood the Fed will lower rates by 0.25% at their March 20 meeting next year.

Update on Federal Reserve Policy (from JP Morgan): This year, markets and the Federal Reserve have repeatedly danced the tango, with markets moving forward in anticipation of early interest rate cuts and then stepping back to realign with “Fedspeak" on inflation and the labor market. As the year draws to a close, the dance has resumed. Last week’s labor data painted a nuanced picture. While job openings fell by more than expected, to 8.7 million, non-farm payrolls rose by 199k, bringing the unemployment rate down to 3.7%. However, this increase in payrolls was anticipated given the return of auto union workers to the workforce. Moreover, wage growth declined to 4% alongside the quits rate, which has softened gradually from its April 2022 peak. While current wage growth is above the Fed’s target level, cumulative real wage growth since the end of the pandemic recession still is negative. As a result, wage pressure seems more in response to past inflation than an indicator of future inflation. However, it is still crucial to acknowledge that despite some recent moderation, the labor market is still very strong, and since the quits rate has stabilized over the last four months, any further moderation in wage growth will likely be gradual. Currently, the futures market anticipates between four and five rate cuts in 2024, starting as early as 1Q. However, unless the labor market weakens significantly and inflation falls back promptly to the Fed's 2% target, the Fed may opt for a more measured pace of easing than the market expects. This week’s FOMC meeting will be critical, with its revised dot plot set to clarify if market sentiment remains more dovish than actual Fed communications.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.