Market Recap – Week ending Jan. 6

Positive Start to Year; CPI Report on Thursday

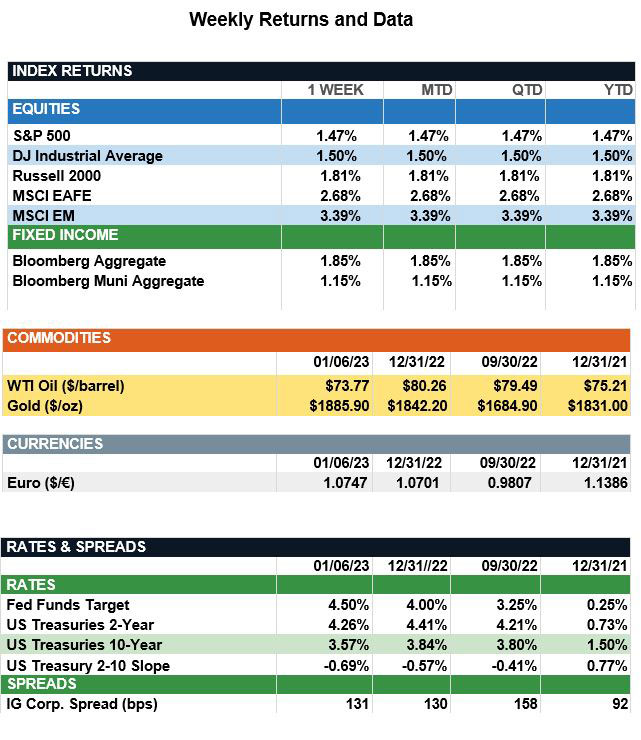

Overview: Stocks and bonds started the year with positive returns last week, led by emerging markets (MSCI EM) and international stocks (MSCI EAFE) stocks up 3.4% and 2.7%, respectively. In the U.S., the S&P 500 index finished 1.5% higher as investors were cheered by lower-than-expected wage growth. Wages, or average hourly earnings, increased 4.6% vs. an expected 5.0% on an annualized basis, suggesting inflation is continuing to ease. Yields were lower on the week, with the 2-year and 10-Year US Treasury yields finishing the week at 4.26% and 3.57%, respectively. These lower interest rates fueled a strong rally in bonds with the taxable Bloomberg Aggregate index up 1.85% and the Bloomberg Muni index up 1.15% in the first week of 2023. In economic data, the employment report for December was strong, with nonfarm payrolls rising 223,000, above expectations for the ninth month in a row. Unemployment declined to 3.5%, a 50-year low. Although this strong labor data would suggest more rate hikes to slow the economy, markets responded positively as wage growth is slowing. According to FedWatch data, futures markets now are pricing in about an 80% chance of a 0.25% (25bp) rate hike at the Federal Reserve’s next meeting concluding Feb. 1. Markets are now expecting a total of three 25bp hikes in total for 2023, which would result in a peak rate of around 5% for the funds rate around the middle of the year. The Fed will continue to monitor inflation data closely and key this week will be the consumer prices (CPI) report due to be released on Thursday, Jan. 12. Expectations are for headline CPI to fall from 7.1% in November to 6.6% in December with core (ex food & Energy) CPI to decline from 6.0% to 5.7% over the month.

The U.S. Labor Market (from JP Morgan): The U.S. labor market was a shining star in 2022 against a dim economic backdrop of tighter financial conditions and recession fears. Although real GDP normally outpaces payroll employment, due to rising labor productivity payrolls grew more rapidly than real GDP growth in 2022, flipping the script on this dynamic. Real GDP growth averaged 2.02% per year from 4Q99 to 4Q19, with payroll employment contributing 0.75% and output per job contributing 1.26%. However, after a pandemic-induced collapse in early 2020, fiscal stimulus and reopening allowed GDP to accelerate rapidly in the second half of 2020 and in 2021, while COVID fears, generous unemployment benefits and weak demographics held labor supply in check. As a result, payroll growth slowed relative to GDP growth. From 4Q19 to 4Q21, nonfarm payrolls fell by 0.97% annualized while GDP grew by 2.04% annualized, leading to a sharp surge in productivity among existing workers and a dramatic surge in job openings. As the economy slowed in 2022, some of this excess demand for labor was relieved. However, last week’s economic reports still showed a very high 1.83 job openings at the end of November for every person unemployed in the second week in December. While we expect both job openings and job growth to fall in the months ahead, persistent excess demand for labor should result in continued job gains, moderate wage growth and a low unemployment rate well into 2023, helping the U.S. economy avoid a deep recession and, perhaps, avoid a recession altogether.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.