Market Recap – Week ending Dec. 30

S&P 500 Closes Down Year; Employment Report on Friday

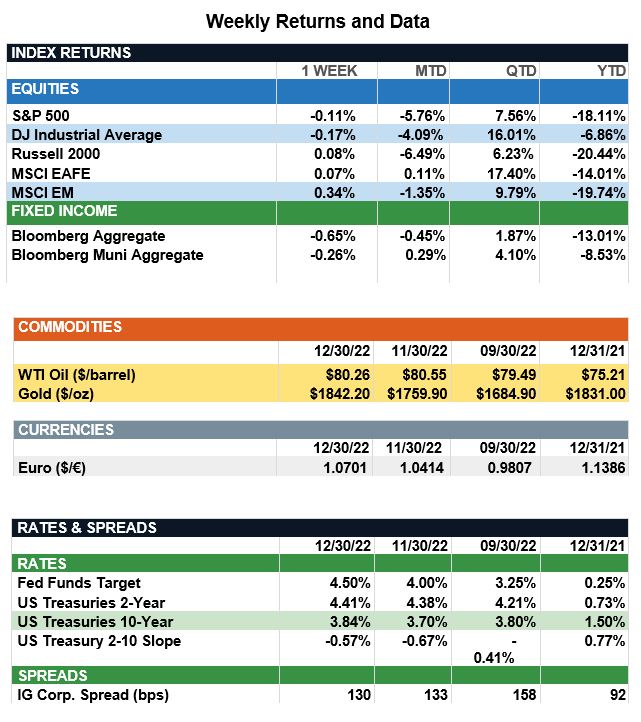

Overview: Global stocks were largely unchanged in the final week of the year as investors closed the books on 2022 and hoped for a better economic outlook for 2023. The S&P 500 Index fell 0.1%, finishing the year 2022 down 18.1%, its worst yearly performance since 2008. Overseas, international stocks were marginally higher in thin holiday trading as concerns about rising COVID-19 cases in China was counteracted by indications of loosening restrictions in the country. Stocks overseas rallied strongly in the final quarter of 2022, benefitting largely from the improved outlook for China COVID restrictions along with a weaker dollar. The U.S. dollar was down about 9% for the quarter vs. the Euro, helping dollar-based returns for both international developed and emerging market stocks. In the bond markets, yields rose with the 2-Year and 10-Year Treasury yields finishing the year at 4.41% and 3.84%, respectively. The sharp rise in yields over the course of 2022 translated to negative yearly total returns of -13.0% and -8.5% for the benchmark taxable bonds and municipal bond markets, with the 2-year Treasury rising in yield from 0.73% to 4.41% for the year. In a similar vein, 10-year Treasury notes rose in yield from 1.50% to 3.84% over the year 2022. As we move forward into 2023, investors will be closely monitoring signs of further Federal Reserve rate hikes as well as the health of the economy. Market expectations currently are for the Fed to raise the funds rate by a total of 0.5%-0.75% (50bp to 75bp) beginning with an expected 25bp hike at their next meeting on Feb. 1, 2023. The first key economic report of the year, the monthly employment report, will come this Friday, Jan. 6. Expectations are for the economy to add 200,000 jobs, with the unemployment rate expected to hold steady at 3.7%.

Recap of the Year 2022 (from JP Morgan): 2022 was a difficult year for the public markets, as positive stock-bond correlations offered investors little to no protection against the macroeconomic backdrop of persistently high inflation, hawkish monetary policy and heightened geopolitical tensions. In terms of asset class performance, commodities led the way in 2022, as the conflict in Ukraine and only gradually improving supply chains boosted commodities prices. Equities struggled in 2022, primarily due to higher rates compressing valuations and a weakening outlook for corporate earnings amid recessionary fears. U.S large cap finished the year down 17.9%, while their small cap peers ended the year down 20.2%. REITs, which had a stellar 2021, felt the pain of tighter monetary policy and declined more than 20% as the demand for real estate cools. In the international markets, DM equity and EM equity declined 13.5% and 19.6%, respectively. The conflict in Ukraine continues to weigh heavily on the European markets, with the UK officially entering a recession and the European Union expected to do so in 2023. Furthermore, the Bank of Japan’s surprise rate hike announcement in early December added further pressure in developed markets. Turning to emerging markets, China continues to dominate the headlines. While policy officials have recently eased COVID-19 restrictions, the country remained in lockdown for most of 2022. Lastly, similar to equities, the bond markets felt the pressure of higher interest rates. U.S. fixed income markets finished the year down as the Federal Reserve holds steady with its hawkish policy stance. Global high yield finished the year down as well, primarily due to a flight to quality and an increase in downgrades.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.