Tax Planning for the Biden Administration

Potential Strategies to Combat Increased Taxes

Many individuals are stuck in a holding pattern as they wait to see what impact the Biden Administration will have on tax regulations. The President has shared what he’d like to see happen, but until those proposals are put into law, it can be hard to know what strategies to take — if any.

From a pure tax planning perspective, no changes to current regulations would be ideal, but even knowing what changes to expect would put filers in a better position, whereas new regulations in late 2021 would offer little opportunity to take action to offset rising taxes.

In several recent articles, Jeffrey Levine, CFP®, CPA discussed the proposed tax changes and potential strategies to combat any adverse effects. Levine is the CPO of Buckingham Wealth Partners and the Lead Financial Planning Nerd for the popular financial website www.Kitces.com. Here are just a few of the more significant changes that could impact your net income going forward.

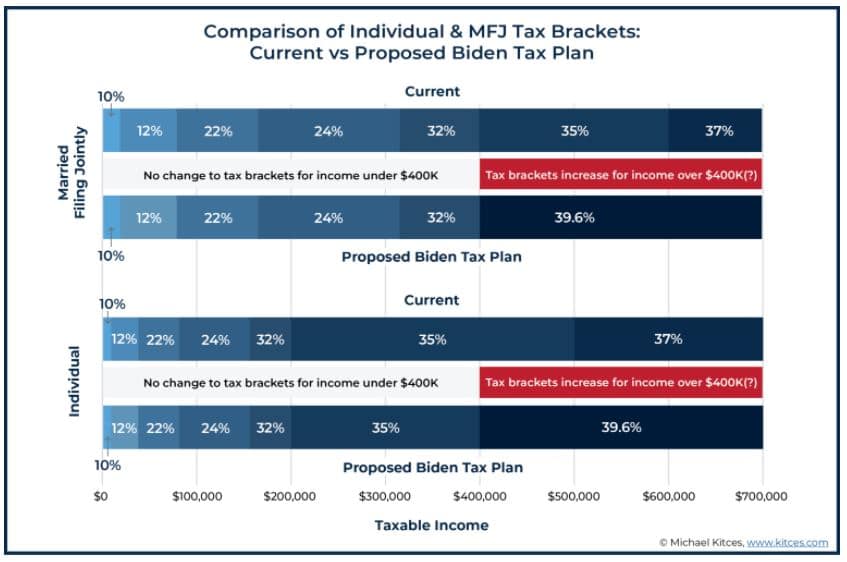

Increased Taxes for Salary Earners Making $400k and Over

If the Biden Administration has their way, an annual income of over $400k will propel individuals and those who are married and filing jointly into a 39.6% tax bracket as compared to the current 35% bracket.

Potential Planning Strategies:

Accelerating Income – To offset a potentially higher tax bracket, Levine recommends taking advantage of current tax laws while they last. That means accelerating income in 2021. You may have a higher tax bill this year, but you could counterbalance even greater tax liabilities down the road.

If you’re a small business owner, you may be in a better position than some to accelerate income and also put off anticipated business costs to 2022. That way you’ll have more deductions to compensate for a potentially higher tax bracket next year. There is one caveat to this approach, however. That’s the potential for the Biden Administration to put a cap of 28% on potential itemized deductions. If this piece of legislation goes through, then taking partial deductions this year may also be necessary to maximize your ability to write off expenses.

Roth Conversions – Converting a traditional IRA or 401(k) into a Roth IRA is one way you can capitalize on a lower tax bracket now if you’re an over $400k earner. Then, if taxes are increased in the future, you’ll already have your assets converted to a tax-free account.

Increased Tax Rates for Long-Term Capital Gains and Qualified Dividends

Those earning over $1 million a year could end up paying ordinary income tax rates on long-term capital gains and qualified dividends.

Potential Planning Strategies:

Investments with Little Tax Implications: Levine recommends looking for minimal tax investments like municipal bonds, avoiding investments that produce dividends and regulating annual sales to stay under the $1 million cap as just a few ways to help minimize your tax liability.

Changes to Estate and Gift Planning Legislation Another proposal that’s looming on the horizon is the reduction of the estate and gift planning exemptions put into effect during the Trump presidency. Current rules allow for $11.58 million in tax-exempt wealth transfer per person, whereas proposed changes will revert that amount to approximately $5.85 million per person.

Potential Planning Strategies:

Maximizing Gifts in 2021: One option, per Levine, is to take advantage of the current rate and donate $11.58 million per individual this year. That’s a solution that takes careful planning — especially for those whose assets are tied up in a business or those with barely enough assets to cover the gift and have enough to live on for the remainder of their lives.

“Stretch” Donations for Couples: Another strategy is to max out your gift this year, while your spouse waits until later. You’ll donate $11.58 million, and then if the exemption goes down, your spouse will still be able to gift $5.85 million later. If you split the $11.58M evenly this year and the exemption goes down, you’ll each have effectively eliminated any opportunity for more gifting in later years.

Should You, or Shouldn’t You? So how do you plan for taxes when you don’t know what regulations will change if any? It’s a question on the minds of many investors trying to maximize their net revenue. On the one hand, if President Biden’s tax proposals don’t go into effect, you might make unnecessary changes that could trigger additional taxes. On the other hand, if the proposals become law, you could regret not taking action while you’re in a more optimal tax situation.

Contact Us for Tax-Focused Financial Planning Solutions We can help you make sense of the planning options available to help offset anticipated increases during the next presidential term — and whether you should take action now or stay the course. Timing is everything when it comes to taxes, so contact us today to schedule an appointment!

Sources: